While it is sometimes true that your insurance premiums decrease as your car gets older, this is not always the case, especially when inflation is high. Premiums tend to increase in line with inflation.

The Bureau for Economic Research (BER) says we can expect inflation to remain at around 7% for the next several months as higher diesel prices and input costs hit consumers. Unfortunately, an elevated inflation rate means increased costs associated with vehicle repairs, and ultimately, insurance premiums.

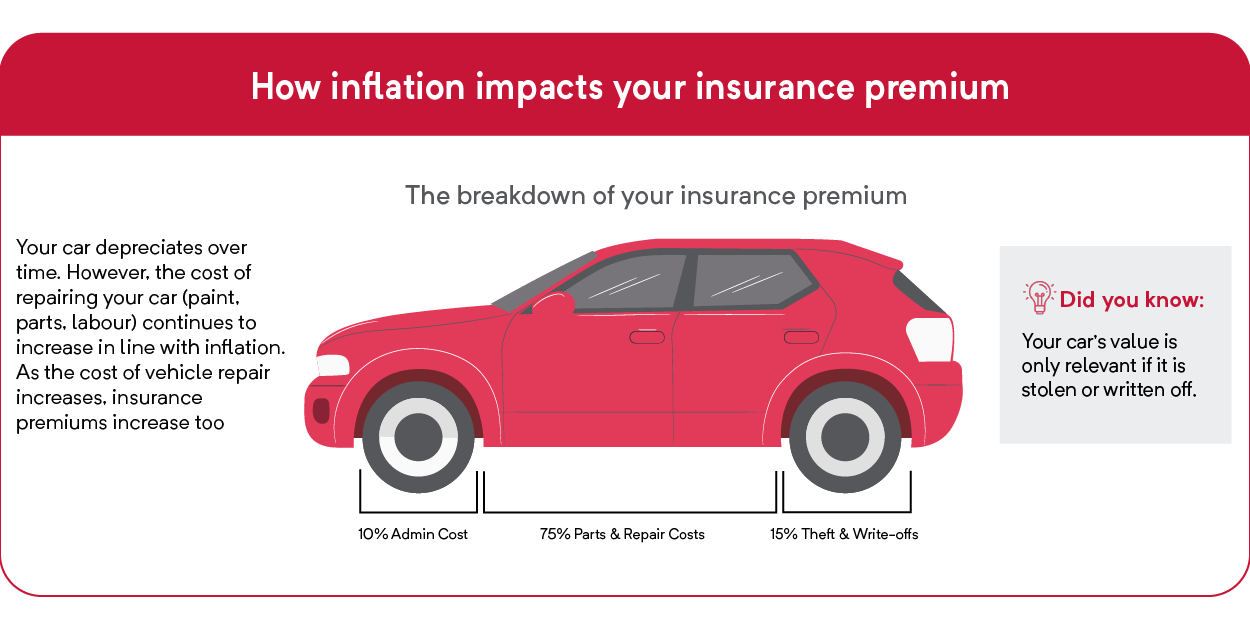

Your car depreciates as it gets older, begins to show more signs of wear, and the mileage increases. However, the cost of repairing your car – the price paid for paint, parts, and labour - continues to increase in line with inflation. So, even if your car is worth less than it was when you bought it, repairs are still costly. For example, if your car side mirror needs to be replaced after an accident, the cost of the mirror and the labour associated with the repair will be high, regardless of how old your car is.

Insurers report that most claims are a result of accident damage. This means the insurance carries a greater risk of paying for accident damage than they do for vehicle theft or total write off. As a result, a greater percentage of your premium goes towards the risk of accident damage.

As the cost of vehicle repair increases because of inflation, it’s likely that the price of insurance premiums will increase too.

![]() Additional factors that increase your Insurance premium

Additional factors that increase your Insurance premium

Your monthly insurance premium is impacted by several factors – some are in your control, and others are not. When it comes to low insurance, shopping around will find you the best price.

Below are some other factors that might increase your insurance premium:

1. Choosing the incorrect excess amount

The excess is the amount you are liable to pay when you are in an accident, or your car is stolen. If you choose a low excess amount, your monthly insurance premiums will be higher. However, if you choose a high excess amount to get lower monthly premiums, be sure that you are in a financial position to pay the excess if your car needs to be repaired or replaced.

2. A history of previous claims

To calculate your insurance premiums, companies look at how often you have claimed in the past. People who aren’t involved in many accidents or who haven’t claimed often will enjoy lower premiums and sometimes even cash-back rewards.

3. Choosing comprehensive coverage

Comprehensive Coverage is the most expensive type of insurance because it covers your vehicle from fire, theft, hijacking, natural disaster, or an accident with another vehicle regardless of fault. In the event of a claim, you are only responsible for the excess to repair or replace your vehicle. If your car is financed, most banks will require Comprehensive Coverage.

4. Driving a luxurious car

Usually, the more luxurious and expensive your vehicle is, the higher your insurance will be. This is because it’s usually more costly to repair or replace these cars.

5. Where your car ‘sleeps’

The neighbourhood you live in impacts your insurance premiums – if you live in a high-risk area, your insurance premiums will be higher. If you park your car overnight in a locked garage, and if you have security features such as a vehicle tracker and an alarm, your insurance premiums might be lower.

6. Using your car for business

If you drive your car for work throughout the day, your insurance premiums will be higher because more time behind the wheel usually means higher risk.

7. Your age and gender

Younger, less experienced drivers usually pay more for car insurance. Coverage for men is usually more expensive than coverage for women because men are seen as a higher risk.

Tough enough for any terrain: Toyota Land Cruiser LC79

Top tips on how to entertain kids on long car rides